- The Skinny on Wall Street

- Posts

- The Skinny On...

The Skinny On...

Deal of the "century"? Plus: why are Japanese equities rocketing higher?

The Wall Street Skinny

February 13, 2026

Kristen gives us a deep dive into the historic shifts behind Japan’s equity market rally, and we’re answering YOUR questions about Alphabet’s 100-year bond issuance!

— Jen & Kristen

The AI notepad for people in back-to-back meetings

Looking for an AI notetaker for your meetings?

Granola is a lot more.

Most AI note-takers just transcribe what was said and send you a summary after the call. Granola is an AI notepad. And that difference matters.

You start with a clean, simple notepad. You jot down what matters to you and, in the background, Granola transcribes the meeting.

When the meeting ends, Granola uses your notes to generate clearer summaries, action items, and next steps, all from your point of view.

Then comes the powerful part: you can chat with your notes. Use Recipes (pre-made prompts) to write follow-up emails, pull out decisions, prep for your next meeting, or turn conversations into real work in seconds.

Think of it as a super-smart notes app that actually understands your meetings.

Download Granola and try it for your next meeting. Free month with code WSS1OFF

100 Year Bonds: The “Deal of the Century”?

We got the following question in our fan mail:

hi! My name is Bethany, I’m from Kansas City. I love listening to the podcast! I’m a future episode could you dive into all these corporate bonds? 100 year bonds in sterling?? What does this mean for US treasuries if anything at all. The bond market is still confusing to me and I’d love to listen to your thoughts. Thanks!

The corporate bonds referenced here are likely Alphabet’s recent announcement of a total of $32bn worth of debt issuance across three currencies: USD, GBP, and CHF. The most exciting part? One of the Sterling-denominated bonds they issued was a bond with a 100-year maturity.

Century bonds don’t happen all that often, so it’s a great opportunity to discuss what they are, who typically issues them, why the most recent issuance in particular is so unique, and the broader implications for the markets as a whole.

For starters, let’s be clear: these 100-year bonds are fixed rate instruments, where issuers can lock in a funding rate that doesn’t change for the next century. For corporate bonds, they price at a spread to the longest maturity sovereign bond available in that market. Given most governments don’t actually issue 100-year bonds, that’s typically a much shorter-dated instrument on paper (in the U.S., a 30-year Treasury; in the U.K., a 50-year Gilt).

However, just because there’s a big difference in maturity on day one doesn’t mean as much as you think. Why? Because the most important metric on our bonds isn’t maturity, it’s duration.

A textbook will define duration for you as the cash-weighted time to receiving all the money from your investment. But in practice, we use it as a measure of a bond’s risk. Investors like to live in the now. Practically speaking, as important as it is to know when you get all your money, it’s even MORE important for investors to know how much money they make or lose TODAY for every 1 basis point change in the bond’s yield over its entire life.

This risk metric is derived from a bond’s duration and is called its DV01: the dollar value TODAY of a 1 basis point move in yields. So, when you think about calculating the present value of future cash flows, you’re discounting cash flows in years 51-100 back by such a steep rate that they are relatively worthless compared to cash flows you’re getting in 1, 5, or 10 years by comparison. As such, the DV01 of a 100 year bond really isn’t that different from a 50 year bond. You can see this evidenced by the flat shape of the long end of the yield curve; investors don’t tend to demand much more term premium for 100 years than they do for 30 or 40 years.

Typical yield curve structure out to 30 years — it’s pretty flat out to 100!

It makes sense intuitively, right? Why worry today about a cash flow you likely won’t even live to see? For better or worse, we have bigger fish to fry before 99 years are up.

That being said, these bonds still have MASSIVE DV01s, which means any small move in rates can mean BIG swings for investors on a mark-to-market basis. They aren’t a great fit for upstart companies that might not be around in a few years, and even less of a fit for investors who can’t suffer massive PNL markdowns on any given day.

So they can be great tool for institutions to fund themselves beyond the foreseeable future. They are typically issued by universities like Oxford, MIT, and UPenn, who have all recently issued 100-year bonds to finance their endowment infrastructure. These are all institutions that have existed well over a century and expect to exist for many more.

Corporations have a much more mixed track record with 100-year bonds. Companies with massive staying power like Disney, Coca-Cola, and FedEx all tapped the market in the 1990s. But tech hasn’t really been a player in the ultra-long end of the curve, with the exception of IBM and Motorola (once a blue chip company that has since faded into irrelevance).

The real question is: who’s going to buy these things? Who wants to tie their money up for a century and not get compensated much more than you’d earn tying your money up for 30 years? And who on earth can withstand the mark-to-market volatility of something with such massive risk?

Ironically, the same type of institutions who typically issue these things, like endowments, and even more so, pension funds and insurance companies with long dated liability profiles. They have known long-term payment needs, and need similarly long-term assets to grow their pile of cash sufficiently to make sure they can fund those future payments.

It is quite rare — basically, unheard of since the dot com bubble — for tech companies to fund themselves with ultra-long debt. But we’ve seen increasingly creative financing structures from hyperscalers, who are starting to tap the debt markets with greater frequency and volume, despite the fact that they generally have cash on hand or revenue streams in the foreseeable future to fund much of their spend.

Now, while we don’t typically think of tech companies as being bond traders, important to realize that the strategic decision to issue bonds with these maturities implies a market view from companies like Alphabet. And that view is:

1) the long end of the yield curve is unlikely to stay at today’s low yields for long, and

2) credit spreads are poised to widen out from current levels.

Basically, “strike while the iron is hot”. After all, issuing fixed rate debt is, implicitly, getting short the corporate bond market from current levels.

The decision to issue in Sterling was specifically in response to UK pension demand for long dated assets, and the deal was more than 10x oversubscribed (meaning, the ratio of interested buyers to available bonds for sale was 10:1). But beyond just the century bonds, all the bonds across tranches that have priced so far have come well inside price talk, meaning they were issued at tighter credit spreads (i.e., richer valuation levels) than anticipated, because investor demand has been so strong.

The broader implications for the fixed income markets are significant.

First: the century bond signals that top-tier tech firms are now competing directly with deeply established institutions and sovereigns for investor capital. This is a huge change from the cash-heavy model that characterized Big Tech for ages. Companies like Alphabet are now behaving more like utilities or infrastructure operators, with long-duration capital needs and business models predicated on decades-long asset lives. If this becomes the new norm, it fundamentally changes how we should think about tech credit risk and valuation.

Secondly: this is only the beginning of a projected wave of bond issuance driven by hyperscaler borrowing. If the trillions of issuance currently projected by the street materialize, we are likely to see spreads widen across the curve, particularly in the long end. According to Morgan Stanley, we’re in for a redux of the late 1990s or 2005, where credit underperforms but doesn’t collapse.

And third, to our listener’s original question: Alphabet is implicitly expressing a view that the long end of the yield curve looks rich relative to fair value. Said differently? Yields look too low.

This is in line with the theme we’ve been discussing all year, that the long end of sovereign yield curves — whether it be the US, UK, Europe, or Japan – simply don’t offer investors sufficient return for tying up their money for extended periods of time. So if the yield curve stubbornly refuses to steepen out, it’s a smart move to issue at lower financing rates while you still can!

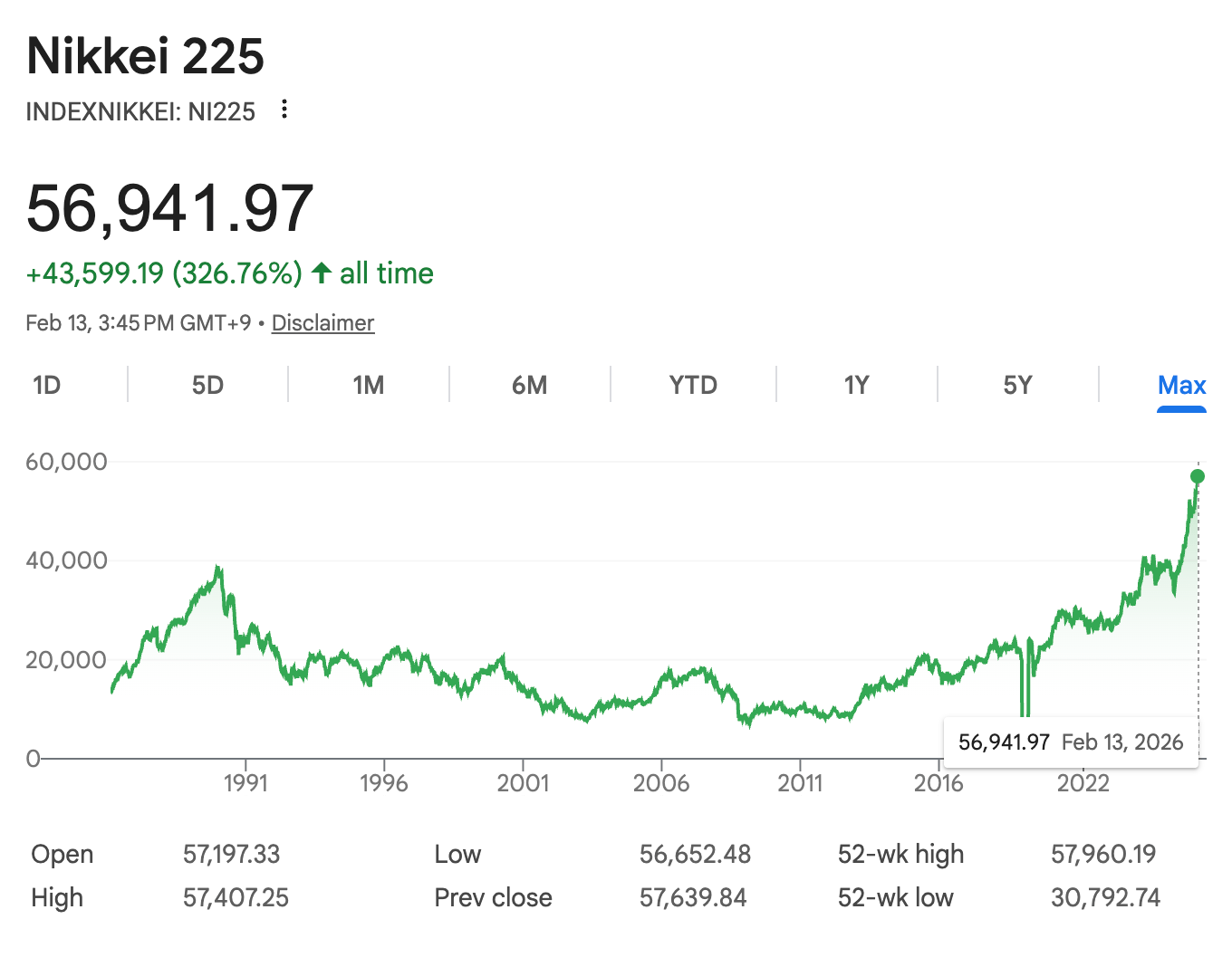

Kristen with essential insight into the rally in Japanese equities

The Nikkei just hit an all-time high. What is happening?

Japan's stock market hasn't been here since the bubble economy of the late 1980s. The Nikkei 225 and TOPIX have both surged to record highs, closing a chapter that investors called "three lost decades."

But this isn't a single-catalyst story. It's the payoff of a reform arc that began over a decade ago with Shinzo Abe.

When Shinzo Abe became Prime Minister in late 2012, Japan was trapped in a deflationary spiral. His response was a sweeping economic program — “Abenomics” —built on three "arrows":

Monetary easing: Massive QE, negative rates, yield curve control

Fiscal stimulus: Infrastructure & cash injections

Structural reform: Corporate governance, tax cuts, labor flexibility

The first two made headlines, with massive bond purchases and government spending. But it's the third arrow, particularly corporate governance reform, that is less-discussed and is our focus today.

A system built for safety, not shareholders

For decades, Japanese corporations were run for employees and stability, not shareholders. Companies sat in keiretsu networks – corporate groups holding each other's shares – hoarding cash and prioritizing employee well being over returns. Boards were dominated by insiders. CEOs were rarely removed for underperformance. Nearly 43% of listed companies traded below book value.

That model worked in the postwar boom, but it became a drag during three lost decades of deflation.

Demographics forced the issue

Japan has an inverted population pyramid: a shrinking workforce supporting an ever-growing number of retirees. Over 28% of the population is 65+. By 2050, there will be just 1.2 workers per retiree. Japan has one of the world's largest pension funds (GPIF, with $1.87 trillion in assets), which recently adjusted their portfolio and doubled their equity allocation to 50%, with a bias for domestic equities. But, here's the thing. You need those stocks to actually perform in order to create value. That's where corporate governance comes in.

Inflation changed everything

Now add inflation. For the first time in 30+ years, Japan has sustained price increases closing in on 2%. Unlike how we currently perceive inflation in the US, for a country like Japan that fought deflation for decades, this is a good thing.

Companies can raise prices for the first time in a generation. Workers are getting real wage increases. Households are moving savings into equities; ¥7.5 trillion flowed into investment accounts in just the first half of 2024. And companies can no longer justify hoarding cash. Uninvested capital now loses real value every year.

Enter Sanae Takaichi

In October 2025, Sanae Takaichi became Japan’s first female PM. She also won a historic supermajority in the February 8th snap elections, giving her the strongest mandate any Japanese PM has held in decades. As Abe's protégée, she's doubling down on his playbook. Her economic program, "Sanaenomics," favors expansionary fiscal policy and strategic investment in sectors like semiconductors, AI, and defense.

The Tokyo Stock Exchange is naming and shaming companies that don't improve capital efficiency. Buffett is buying Japanese stocks. It's all converging.

The bottom line

Ultimately, this isn't a momentum trade or a single-catalyst pop. It's the culmination of a decade-long structural shift from a market that prioritized stability over returns to one that's finally being rewired to increase shareholder value.